Table of Content

The funds can come from the borrower’s savings, cashed-in investments, gift funds from others , even down payment assistance . Bankrate.com is an independent, advertising-supported publisher and comparison service. We are compensated in exchange for placement of sponsored products and, services, or by you clicking on certain links posted on our site. Therefore, this compensation may impact how, where and in what order products appear within listing categories. While we strive to provide a wide range offers, Bankrate does not include information about every financial or credit product or service. Browse through our frequent homebuyer questions to learn the ins and outs of this government backed loan program.

A VA borrower typically makes NO down payment unless they are trying to reduce the amount of the VA loan funding fee, which reduces depending on how much down payment you make. Younger buyers are more likely to purchase a home with less than 20% down. Sixty-three percent of Gen Z and Millennial buyers make a down payment of less than 20%. Far fewer Boomers and Silent Generation buyers put down less than 20% down, just 41%.

You are now leaving the Cherry Creek Mortgage website

What do the FHA home loan rules say about such transactions and how such funds can be used? The answer is in HUD 4000.1, which addresses a variety of such sources. That can include proceeds from the trade-in of a manufactured home, the proceeds from the sale of real estate, or the proceeds from the sale of private property. While it might not be your first choice, one option is to consider extending your timeline for buying to give you more time to save money for a down payment. Or, you can look for other ways to increase your cash flow, such as taking on a second job or starting a side hustle. Seasoned funds are those that have been in the home buyer’s bank account for a period of time.

This is important because prior to the rule, most borrowers could not have their rental history considered as a positive factor. FHA loan rules are specific and clear in these areas to insure fairness and to preserve the integrity of the home buying process with FHA loan funds. If you are planning to use a credit card to make your payment, please check with your credit card company to find out if any fees (e.g. cash advance fees) will apply to your transaction. Tell your lender you’re receiving a gift if there’s an expectation to pay back the funds. Know the monetary total of gift funds for any applicable tax reporting.

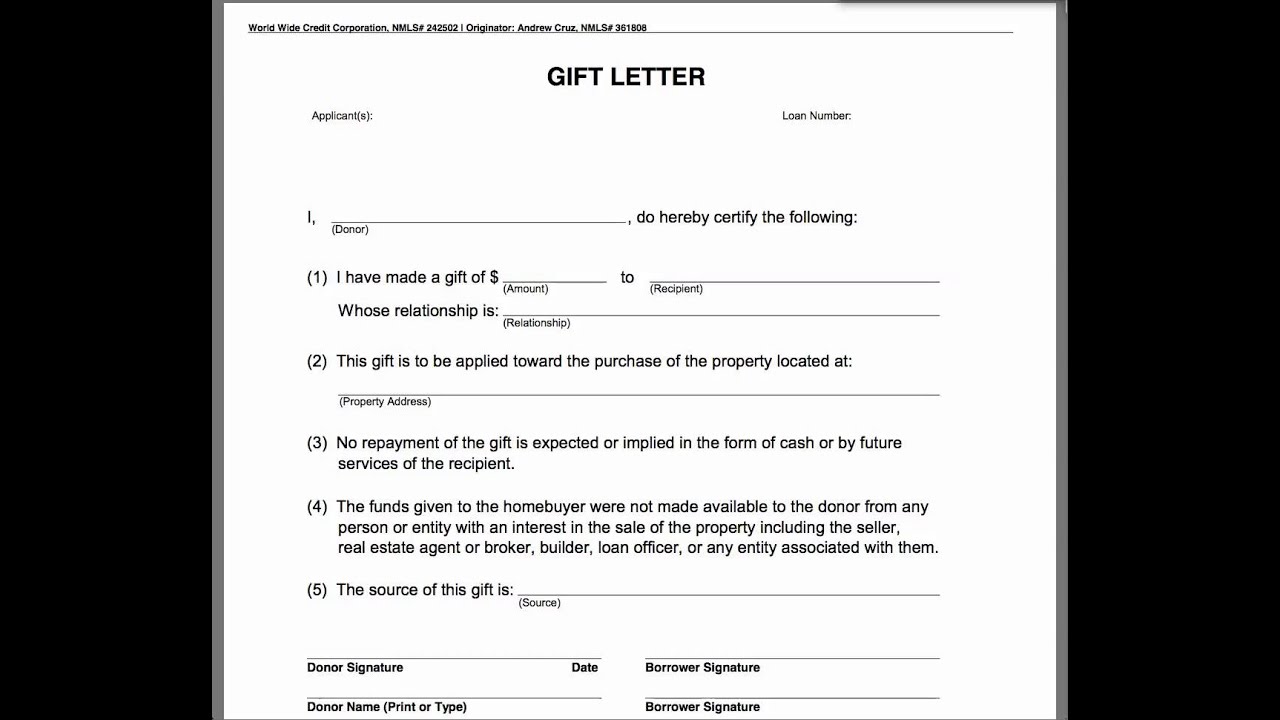

Documenting a Down Payment Gift

In the last months of 2022, the FHA and HUD issued a mortgagee letter announcing a crucial change in FHA loan approval policy. The FHA Single-Family Home Loan program was modified in 2022 to permit lenders to submit positive rental history as a factor in home loan approval. 3) Your rental history can help boost your credit if you pay on time and have a pattern of doing so. But the catch is that your landlord must report this activity to the credit agencies. You'll need a minimum of 12 months of on-time rent and utility payments; anything less can seriously hurt your chances for loan approval. What if you can't come up with the entire down payment on your own?

FHA mortgages, by comparison, are much more available to typical house hunters with their low 3.5% down payment requirement in typical cases. You may be required to make a larger down payment if your credit score is too low. The VA One-Time Close is a 30-year mortgage available to veteran borrowers.

Financial Planning Tips for New Home Buyers

Down Payment Assistance programs, sometimes referred to as grants, can provide homebuyers with funds to cover up front and closing costs when buying a house. Borrowers will need to meet the eligibility requirements of the specific program they'd like to use. Credit scores, household income, family size, and homebuyer education requirements will likely be factors. FHANewsblog.com is a private company, not affiliated with any government agency, is not a lender and does not offer to make loans. The opinions presented on FHAnewsblog.com should not be construed as representing the official opinions of any government agency. We do not offer or have any affiliation with loan modification, foreclosure prevention, payday loan, or short-term loan services.

For the gift’s receiver, make sure you document everything along the way so you have everything at hand if you ever need to rely on it. The IRS imposes a gift tax on certain monetary gifts and this tax is paid by the person donating the money, rather than the one who receives it. As of 2022, you could give up to $16,000 to any one person without incurring the gift tax.

How much should I put down on a house?

Many lenders will already have templates in place for their borrowers and additional parties involved, such as gift-givers. Repaying money that was initially documented as a down payment gift is considered mortgage fraud, which is a crime that can result in serious legal ramifications. Mistating gift funds can also put your loan qualification in jeopardy, as all forms of lending need to factor in your debt-to-income ratio. Even though lenders do allow gift funds, they also require mortgage applicants to disclose the source of these funds.

The posted content contained on FHAnewsblog.com is for general information purposes only and is accurate and true to the best of our knowledge. The information should not be seen as financial advice and you should consult with a licensed mortgage professional , prior to taking any action. FHAnewsblog.com assumes no responsibility for errors or omissions in the contents on the Service. Borrowers with FICO scores that fall below 579 are required, according to FHA loan rules, to pay more money down.

The good news for the remaining majority is that there are other possibilities available for when you’re facing low down payment funds. While traditionally gifted for first-time buyers needing help with their entire down payment, a borrower can use gift funds toward a second home. However, if the buyer uses a down payment gift to purchase a second home or investment property, they are required to pay at least 5% of the down payment and the rest can be gifted. This is a question that commonly comes up among borrowers who are receiving gift money from their parents for their first home down payment. What can influence the amount gifted is the nature of the mortgage, the borrower’s credit, and subsequently, the down payment amount.

Bankrate is compensated in exchange for featured placement of sponsored products and services, or your clicking on links posted on this website. This compensation may impact how, where and in what order products appear. Bankrate.com does not include all companies or all available products. For both conventional and FHA loans, the total amount of the down payment can be gifted, in most cases. It might seem odd that there are restrictions around who can give someone cash for a down payment. Cash can come with strings attached, which might affect the borrower’s ability to repay the mortgage.

Domestic partners and fiancés are also eligible to give funds for a down payment. If your family decides to help you out with a down payment gift, you should be extremely happy. However, like any large financial move, there are some rules and regulations to consider. Perhaps the most important is for the giver of the gift, as they’ll need to account for that money on their taxes.

We do not offer or have any affiliation with loan modification, foreclosure prevention, payday loan, or short term loan services. Neither FHA.com nor its advertisers charge a fee or require anything other than a submission of qualifying information for comparison shopping ads. We encourage users to contact their lawyers, credit counselors, lenders, and housing counselors.

No comments:

Post a Comment