Table of Content

Lenders require you to provide some detailed documentation any time a down payment gift is changing hands. The reason banks prefer these sources for a down payment gift is because they are more provable than, say, a stranger on the street who gave you money. It also indicates to lenders that you and your family actually have enough money to afford the loan. Credit card cash advances are not in the same league as payday loans, but the interest rates can be higher than you might expect.

If the buyer is planning to pay back the funds, that money was loaned not gifted, and then the lender is required to factor that into the debt-to-income ratio. This is to ensure that you can actually afford your mortgage payment. Withholding information about your down payment sources could put your loan qualification at risk, and even more importantly, it’s considered mortgage fraud, which is illegal. For conventional loans, so long as you’re investing a minimum of 20% or more as the down payment, all of the funds can come in the form of a gift. However, if your down payment is less than 20%, you’ll then be required to pay a portion of that money from your own pocket.

How do I prove I received the gift money?

With a 20% down payment ($60,000), you’d borrow $240,000, and your monthly payment would be $1,548. The following payment scenarios exclude additional fees and costs such as taxes and insurance. The more money you pay upfront, the less you have to borrow from the lender, and the lower your monthly payment will be. Create a free Bankrate account to get expert advice, personalized lending offers and other resources tailored to your unique financial goals.

FHA mortgages, by comparison, are much more available to typical house hunters with their low 3.5% down payment requirement in typical cases. You may be required to make a larger down payment if your credit score is too low. The VA One-Time Close is a 30-year mortgage available to veteran borrowers.

FHA Home Loan Down Payment Rules: Cash To Close Sources

Conventional-loan requirements include extra steps If the down payment is made up of gift money and the borrower’s own money. In that case, the relative or partner must prove that they have lived with the homebuyer for the past 12 months and will continue to live together in the new house. The minimum down payment required on an owner occupied purchase is 5% down regardless of how many homes you have owned. Whether you are buying your first home or your 10th home you are only required to put down a minimum of 5%. This down payment can come from your own cash, gift from family or can be borrowed from a loan or line of credit. Many people who can afford the monthly mortgage payments and have reasonable credit will qualify.

Other programs, however, will also allow gifts from a charitable organization or a non-blood relative. While it’s recommended to always speak with your lender for information on acceptable donors, below are a few common types of mortgage loans and who qualifies as a gift donor under each program. Depending on the type of mortgage you’re getting, there are different rules regarding who can provide a down payment gift to you. When applying for a mortgage loan, the lender needs a clear picture of your financial situation. This process known as underwriting includes collecting information about your employment, income, and assets.

What is a down payment on a house?

This is why a lender will ask for copies of your most recent bank statements. The purpose of reviewing your bank statements is to ensure you have enough in reserves for mortgage expenses. But sometimes, a family member offers to pay these expenses as a gift to you.

We do have some private lenders that will go as high as 85% but generally you are looking at a maximum of 80%. We often get asked how much a down payment do I need for a mortgage or how much equity can I refinance out of my home. FHA.com is a privately-owned website that is not affiliated with the U.S. government. The Consumer Financial Protection Bureau reports payday loans can cost as much as $15 per $100 loaned, and that may be before late fees and other add-on charges.

Loan Programs

A downpayment is required 100% of the time for new purchase FHA loans and your down payment amount may be affected by your credit scores. Expect to make a minimum down payment of 3.5% if your credit score meets FHA and lender standards; all others will be required to pay a minimum 10% down. When it comes to home buying, 20% or higher is the standard mortgage down payment size that most lenders would ideally prefer. However, things are much different today than they have been in the past, as FHA loans and other proprietary mortgages often have much lower down payment requirements.

Money from the sale of personal property can be used for your FHA home loan closing costs and down payment if the following criteria can be met. Lenders use a standard formula to calculate the monthly payment that allows for just the right amount to go to interest vs. principal in order to precisely pay off the loan at the end of the term. You can use our calculator to calculate the monthly principal and interest payment for different loan amounts, loan terms, and interest rates. The content on this site is not intended to provide legal, financial or real estate advice. It is for information purposes only, and any links provided are for the user's convenience.

The good news for the remaining majority is that there are other possibilities available for when you’re facing low down payment funds. While traditionally gifted for first-time buyers needing help with their entire down payment, a borrower can use gift funds toward a second home. However, if the buyer uses a down payment gift to purchase a second home or investment property, they are required to pay at least 5% of the down payment and the rest can be gifted. This is a question that commonly comes up among borrowers who are receiving gift money from their parents for their first home down payment. What can influence the amount gifted is the nature of the mortgage, the borrower’s credit, and subsequently, the down payment amount.

Lenders want to protect themselves against default by making sure the gift money is what it appears to be (e.g. a gift, not a loan) and the borrower can afford the mortgage. If the borrower gets a down-payment loan from a co-worker and calls it a “gift,” their debt-to-income ratio rises, which can affect their ability to repay their mortgage. So, to protect themselves, the GSEs that back mortgages and United States Department of Housing and Urban Development have created rules for donor eligibility. The minimum down payment required for a conventional loan is 3%. But still, a 20% down payment is considered ideal when purchasing a home. Borrowers wishing to purchase a home with an FHA loan may need some help with the down payment.

FICO scores between 500 and 579 require 10% down instead of 3.5% down. Lender standards will often apply above and beyond this; borrowers should not be surprised to find higher FICO score requirements apply depending on the lender. FHA down payment money cannot come from unapproved sources such as payday loans, cash advances, any indebtedness that is considered “non-collateralized”. Borrowers will need to discuss their down payment sources with the loan officer to insure that both FHA standards and lender requirements are met in this area.

The amount you borrow with your mortgage is known as the principal. Each month, part of your monthly payment will go toward paying off that principal, or mortgage balance, and part will go toward interest on the loan. Do you know how your chosen FHA lender will calculate your down payment? Knowing before you apply can help plan and save for this and other required closing costs.

FHA Down Payments for Homebuyers

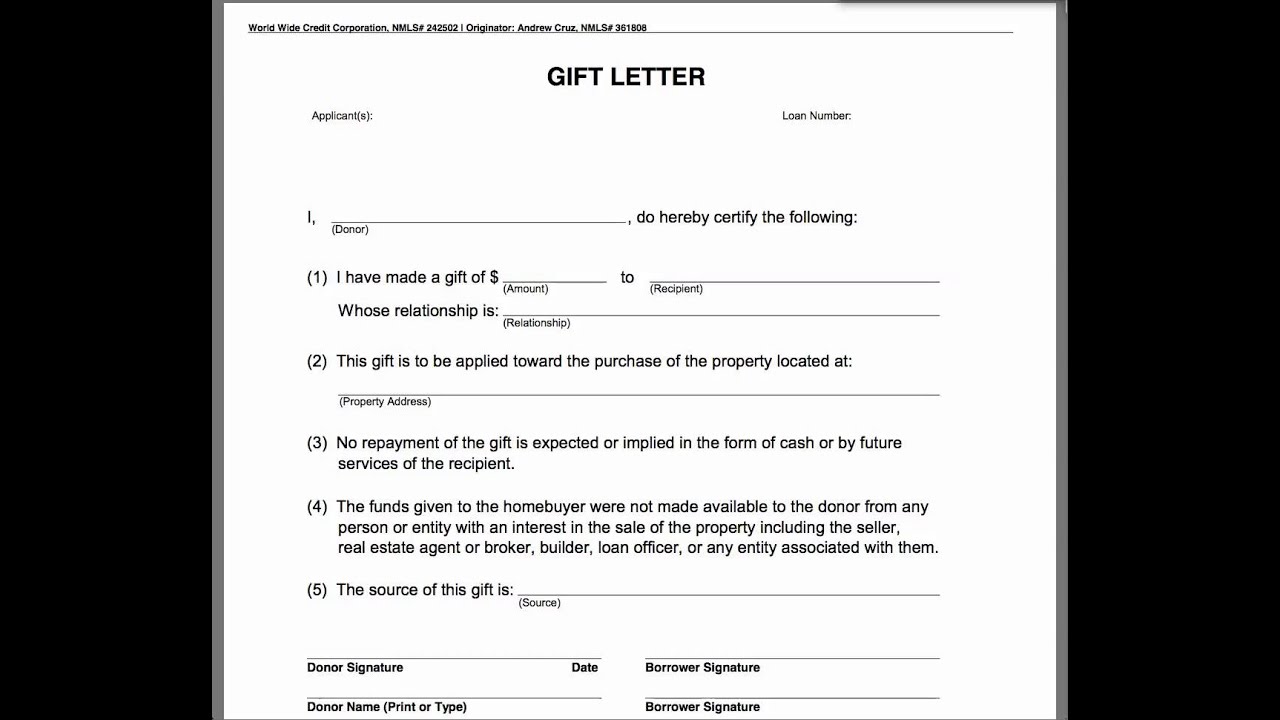

If you’re thinking of going this route, it might be a good idea to crunch the numbers first to find out how it may impact your tax liability when you file. The lender needs documentation of the deposit of sale proceeds. If money is seasoned, you may be able to avoid gift documentation. The more money you put down as part of your down payment, the stronger your loan-to-value ratio. Both the giver and the homebuyer must sign the letter, which doesn’t have to be notarized.

In addition to the $16,000 annual exclusion, some donors may need to be mindful of the $12,060,000 lifetime gift tax exclusion limit set according to IRS Estate Tax for 2022. The person receiving the gift will not be responsible for any tax liability, but the gift giver may be liable if the amount exceeds the gift tax exclusion limit. For a gift that exceeds that amount, the donor must file a gift tax return to disclose the gift. “I/We [name of donor] have gifted [($) dollar amount] to the borrower [name of borrower], my/our . With a typical fixed-rate loan, the combined principal and interest payment will not change over the life of your loan, but the amounts that go to principal rather than interest will.

No comments:

Post a Comment